REITs are primarily valued according to their ability to provide a steady and increasing stream of quarterly dividends. For example, AREIT’s share price has increased by +35% since IPO while FILRT has lost -55%, reflecting its reduced dividends. Another way of looking at REITs is the quality of the properties that they own. As the saying goes in real estate; its location, location, location.

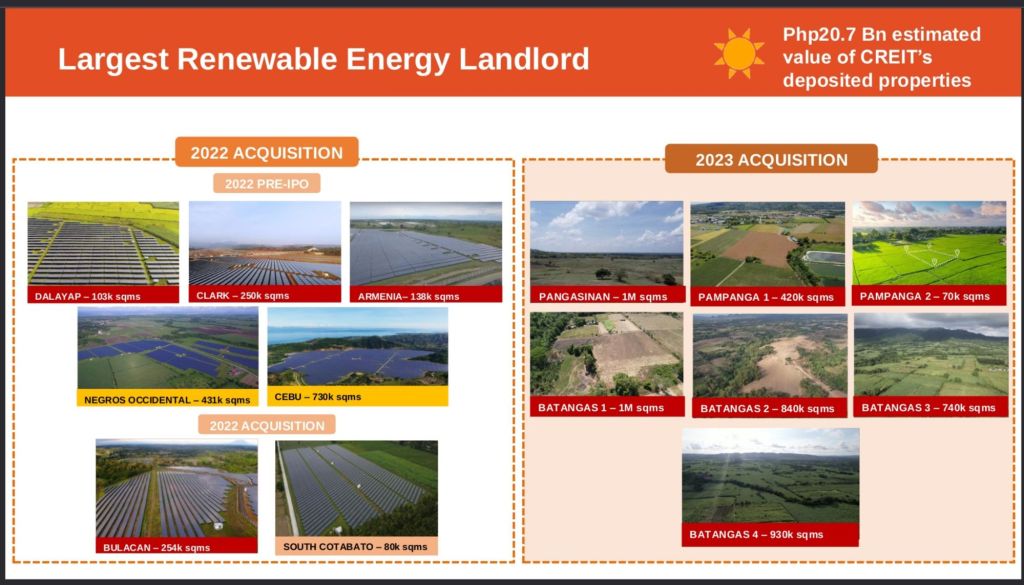

A driver of value that may be overlooked by investors is the future worth of a REIT’s freehold land. I thought about this upon seeing one of Oliver Tan’s interview in the course of CREC’s recent IPO. He is the CEO of CREIT as well. Investors of CREIT would know that their properties consist of both leasehold and freehold land which are leased to solar plant operators. Based on their 2023 acquisition, they are leaning more towards purchasing freehold land. Relative to other types of property, CREIT would be buying these idle, non-commercial, non-agricultural lands at a “low” price now. In the long term, after the life of the solar plant lessee of around 25 years, these large tracts of freehold land could be sold to developers for a significant sum and provide investors with a fat special dividend.

Another advantage of freehold land is that, unlike buildings, it appreciates in value over time allowing CREIT to borrow more when their deposited properties are appraised higher in the future. In their most recent financials, they have allowable borrowings of P9.2 billion using a 70% leverage limit on P20.7 billion of deposited properties and P5.3 billion of debt.

These factors likely led SM Investments Corp. (SMIC) to buy a significant chunk of CREIT shares. This would be a better use of funds compared to just regular land banking. In addition, AREIT recently purchased 276 hectares of Zambales land to be leased to a solar plant as well. PREIT could possibly head in this direction too given that PAVI, its sponsor, is building solar plants in 3 provinces.