I’ve just attended the webinar hosted by COL Financial’s April Lee-Tan with Kerwin Tan, director and treasurer of Robinsons Commercial REIT (RCR). Fortunately COL uploaded it on their Youtube channel so here it is:

I always appreciate companies who reach out to their minority shareholders so kudos to RCR. The first takeaway is the recent announcement that sponsor RLC will be infusing 9 Robinsons Malls this year, subject to shareholder and regulatory approval. Post infusion, RCR’s EBITDA will be approximately 50-50 offices and malls. I think this is great considering the challenges faced by the office sector particularly AI’s impact on the BPO industry. Malls also derive variable rent in the form of a percentage of tenants’ sales so this provides an upside to future dividends, particularly in Q4, when malls are packed with Christmas shoppers.

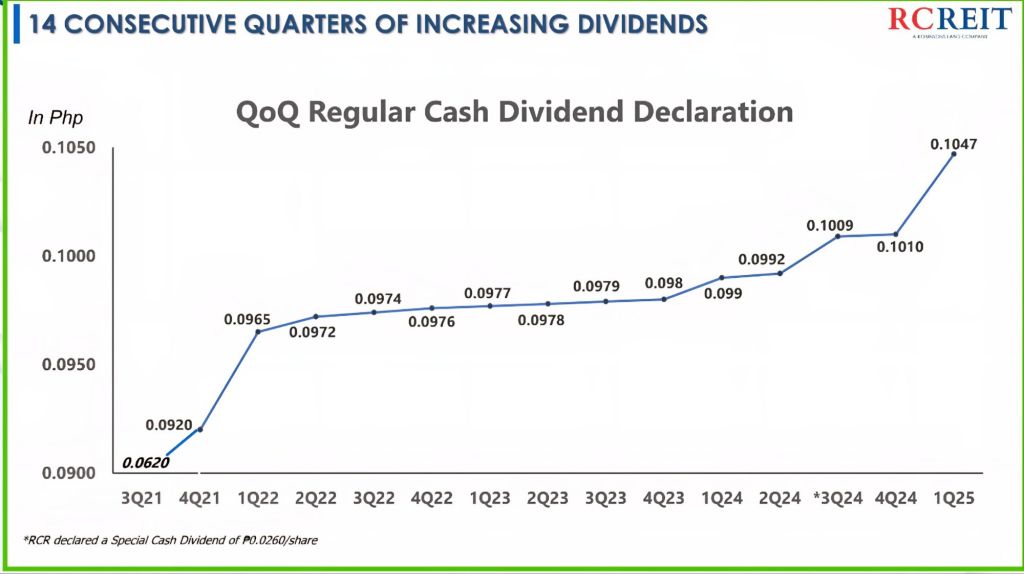

Here is a slide of RCR’s dividends:

Kerwin emphasized that future asset infusions will be accretive to dividends so RCR can most likely maintain and increase the dividends per share going forward.

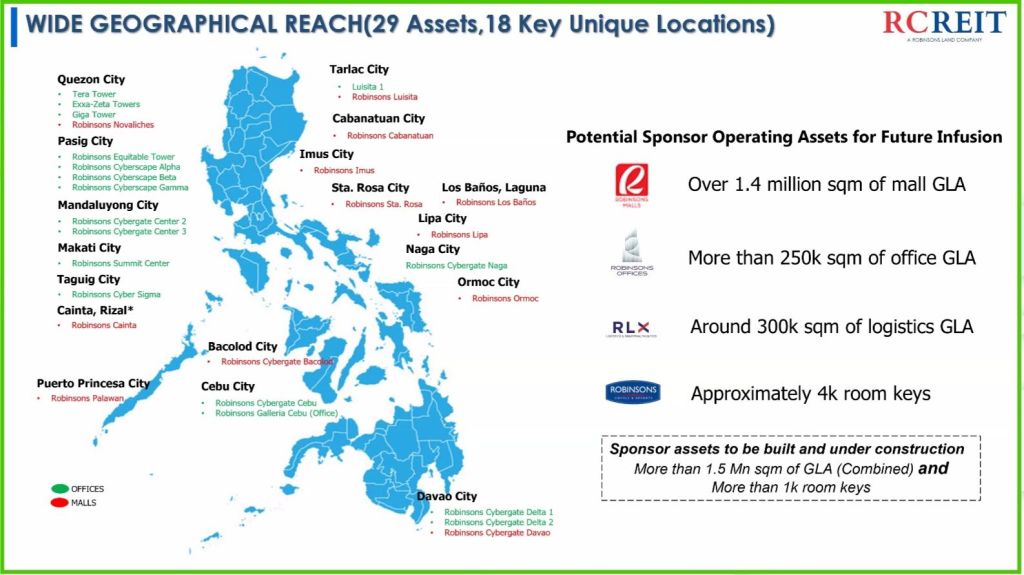

In terms of RCR’s geographic footprint and growth potential, check this particular slide:

RCR only has around 1/3 of RLC’s current operating assets. Not only that, RLC is building more than 1.5 million sqm of GLA, spending approximately P125 billion until 2030. I am particularly keen on the RLX Logistics’ and Robinsons Hotels & Resorts’ assets – hopefully they will infuse some of it into RCR soon for further diversification. Kerwin mentioned that RLX facilities have high margins so having these as part of RCR in the future will be dividend accretive too.

Overall, the impression I got is that RCR is commited to growth so AREIT better watch out. A large and diversified RCR will encourage more foreign funds to invest in them, especially if they become part of the index. For us shareholders, more asset infusions translate to fatter quarterly dividends that are more resilient and more protected from risk.